5 minutes read

Buying a House Before Marriage: The Pros and Cons

Buying a home before marriage? Learn the key pros and cons of co-owning property with your partner.

KB

Kyler Bruno

04/22/2025

More and more unmarried couples are choosing to buy a house before marriage. With rising home prices, shared financial goals, and a shift in societal norms around relationships, buying a home before marriage is no longer rare it’s practical.

But before you take this exciting step with your partner, it’s crucial to understand both the opportunities and the risks involved.

Why Couples Buy a Home Before Marriage?

- Affordability: Combining incomes makes qualifying for a mortgage easier.

- Life goals: Couples want to grow together without the legal formality of marriage first.

- Investment mindset: Real estate is often a better investment than rent.

Now, let’s break down the pros and cons of buying a house before marriage and what you absolutely need to prepare for.

Pros of Buying a Home Before Marriage

1. Build Equity Early

The sooner you own property, the sooner you start building wealth. Equity can be used for future financial goals: home upgrades, investment properties, or retirement.

2. Split Financial Burden

You can share the mortgage, utility bills, taxes, and repairs freeing up your individual income for other priorities like travel, education, or savings.

3. Potential Tax Savings

Homeowners may benefit from mortgage interest and property tax deductions. Unmarried couples can strategically divide these deductions such as letting the higher earner claim more.

4. Flexible Financing

If one of you has better credit or income, that partner may qualify for a lower rate. However, ownership and mortgage details must be clearly documented.

5. Relationship Readiness Check

Buying a home together is a real-world relationship test. It reveals how you both manage money, stress, and long-term planning.

Cons of Buying a Home Before Marriage

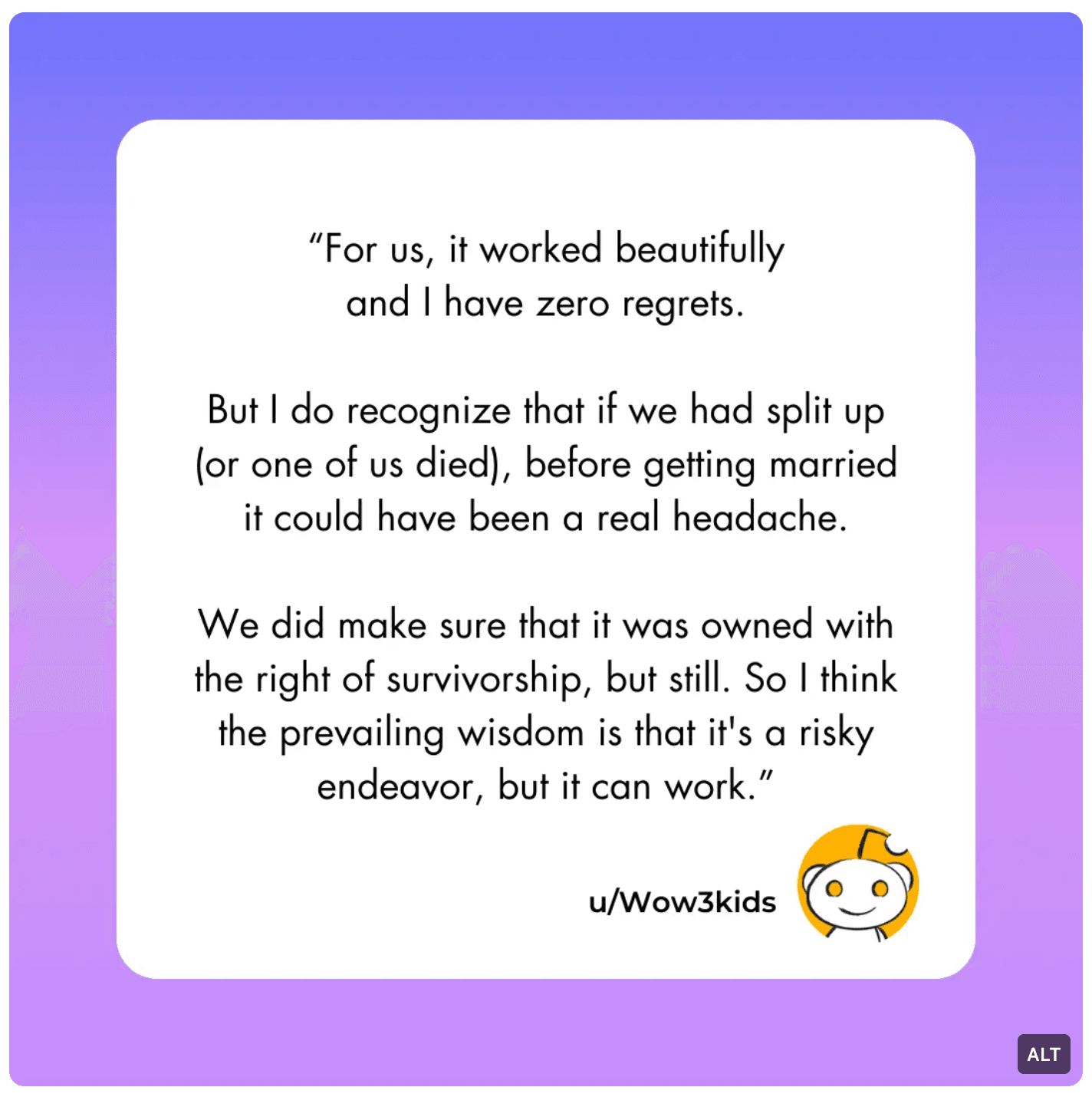

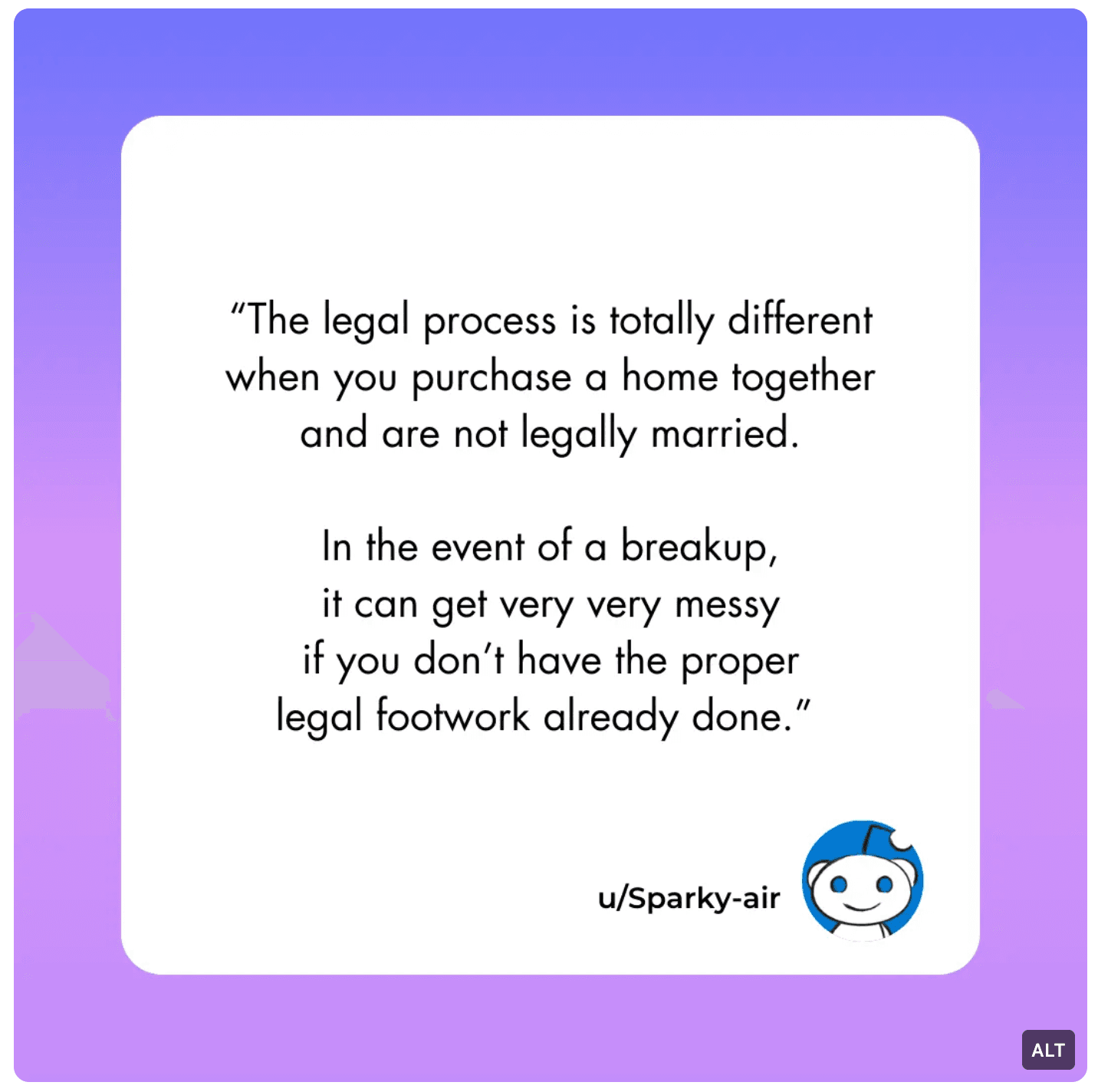

1. Lack of Legal Protections

Marriage comes with default legal protections. Without a formal agreement, ownership disputes could turn messy and expensive in court.

2. Unequal Contributions

If one partner puts in a larger down payment or pays more monthly, it could create resentment especially if the relationship ends.

3. Breakup Risks

A breakup could force a premature sale possibly at a financial loss. Emotions can cloud smart decisions if plans weren’t made in advance.

4. Credit Impact

If both partners co-sign, one’s missed payments or financial mishaps will affect the other’s credit score and financial standing.

5. Complications if You Marry Later

In some states, the property may or may not become “marital property” after marriage. It’s best to clarify this early with legal help.

6 Key Considerations Before You Buy a House Before Marriage

To protect your relationship and your investment, here’s what you must discuss and plan for.

1. Create a Legal Agreement (Cohabitation Agreement)

Don’t rely on verbal understandings. Work with a real estate attorney to define:

- Ownership shares

- Mortgage & utility splits

- Responsibilities for repairs

- Exit strategies (if one partner wants to sell, move out, etc.)

Also consider a prenuptial agreement if marriage is on the horizon to avoid future property disputes.

Consult a real estate attorney before closing. It’s worth the peace of mind.

2. Decide on Ownership Structure

- Joint Tenancy with Right of Survivorship: Equal ownership, survivor inherits automatically.

- Tenancy in Common: Unequal shares allowed, each owner can leave their share to someone else.

Choose based on financial contributions and future intentions.

3. Be Financially Transparent

Discuss credit scores, income, debts, and future financial goals. Determine:

- Who’s applying for the mortgage

- How to divide monthly costs

- What happens if one of you loses your job

💡 Pro tip: If only one name is on the loan, a cohabitation agreement should still outline each partner’s rights and responsibilities.

4. Plan for the “What-Ifs”

It’s uncomfortable but critical to plan for:

- Breakups

- Illness or death

- Market crashes

Update home insurance and consider life insurance to protect the mortgage if one partner passes away.

📌 Document all contributions and keep records & these protect both of you.

5. Hire the Right Professionals

- Real estate attorney: Draft agreements and ensure legality.

- Financial advisor: Optimize your tax benefits and plan your budgets.

- Estate planner: Update wills or trusts for inheritance clarity.

🧠 Smart planning avoids emotional and financial fallout later.

6. Communicate Often

Revisit key questions:

- Are you both planning to live here long-term?

- What happens if one wants to sell or move?

- Will you renovate or upgrade? How will that be funded?

Open, honest, ongoing conversations help avoid assumptions or hidden expectations.

💡 Bonus Tip: Reduce the Financial Pressure

Buying a house before marriage doesn’t have to drain your bank account.

At WithJoy.AI, we help homebuyers reclaim up to 70% of the buyer agent commission as a cash rebate putting thousands back into your hands. This can ease the upfront costs, help cover closing, or furnish your new space together.

💸 Get your rebate and reduce the cost of homeownership with WithJoy.AI.

✉️ Stay Informed. Stay Smart.

Want more tips like this? Subscribe to our newsletter to get:

- Smart homebuying strategies

- Legal & financial planning tips

- Real-life stories from first-time buyers & more!

Final Thoughts: Build on Solid Ground

Buying a house before marriage is both a financial investment and a relationship milestone. With the right planning and transparency, you can turn this into a secure and rewarding step in your journey together.

Here’s to making smart decisions together.

🔑 Don’t just buy a home, build your future smartly. Start with WithJoy.AI .

Related Guides

Top Buyer's Agent Commission Questions, Answered

Answers to top buyer's agent commission questions

KB

Kyler Bruno

07/12/2025

Can You Buy a House with a Credit Card?

Can you buy a house with a credit card? Learn the risks, expert tips, and real alternatives.

KB

Kyler Bruno

07/11/2025

Key Insights from NAR’s 2025 Report

Top 7 takeaways from NAR’s Home Buyers and Sellers Report 2025

KB

Kyler Bruno

07/29/2025

Full Service Home Buying - WithJoy.AI

Find Your Home Today

The future is here. Buy your next home WithJoy.AI

Trending Neighborhoods

Best Places to Retire

Best Affordable Areas Near Seattle

Best for Young Professionals

Best Family Neighborhood Seattle